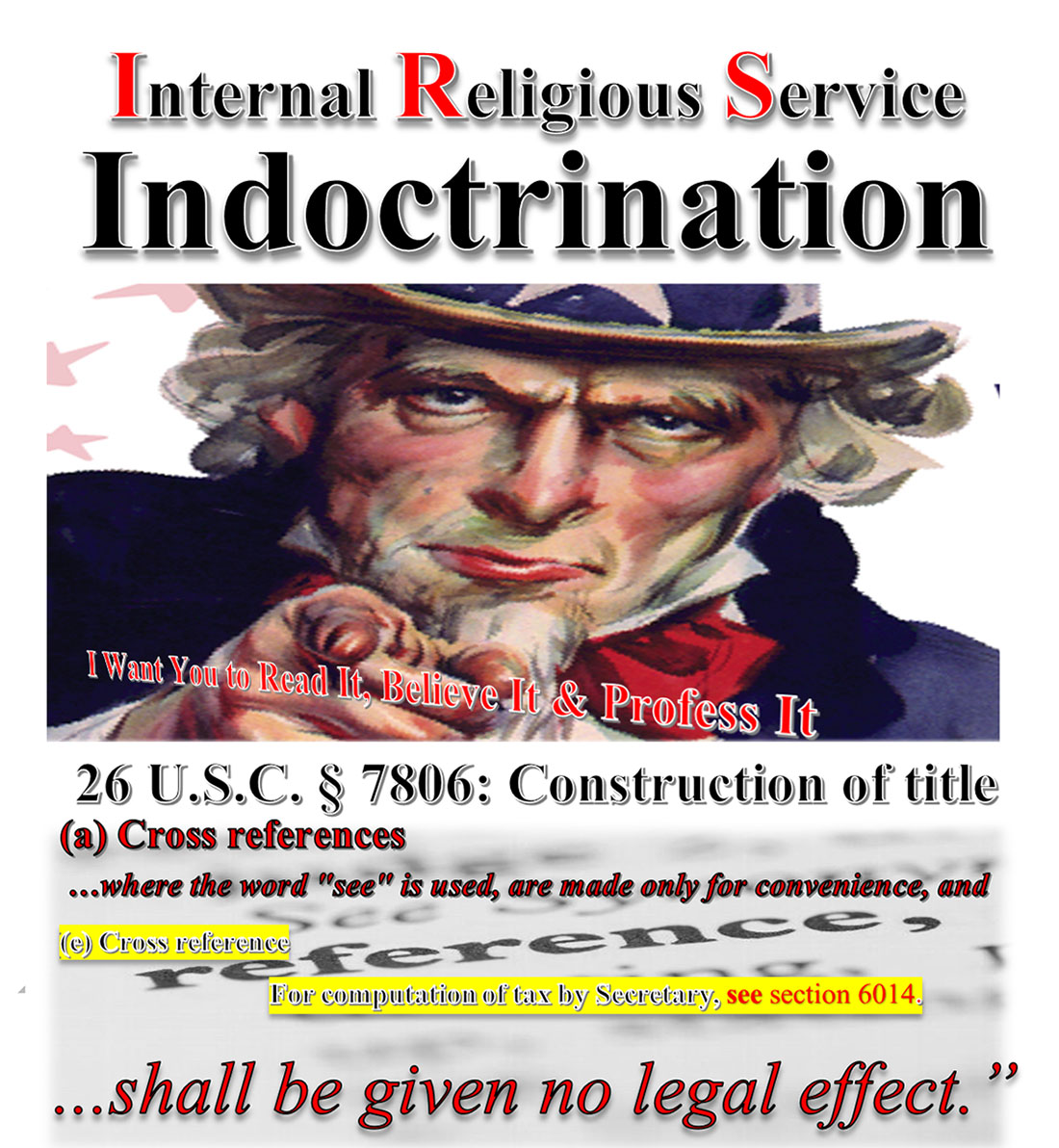

Where the word “see” is used in the cross reference of 26 U.S. Code § 3 – Tax tables for individuals are made only for convenience, and in so doing 26 U.S. Code § 6014 – Income tax return – tax not computed by taxpayer; shall be given no legal effect pursuant to 26 U.S. Code § 7806(a).

26 USC 3: Tax tables for individuals

Text contains those laws in effect on May 1, 2016

Title 26-INTERNAL REVENUE CODE

Subtitle A- Income Taxes

CHAPTER 1- NORMAL TAXES AND SURTAXES

Subchapter A- Determination of Tax Liability

PART I- TAX ON INDIVIDUALS

3. Tax tables for individuals

(a) Imposition of tax table tax

(1) In general

In lieu of the tax imposed by section 1, there is hereby imposed for each taxable year on the taxable income of every individual-

(A) who does not itemize his deductions for the taxable year, and

(B) whose taxable income for such taxable year does not exceed the ceiling amount,

a tax determined under tables, applicable to such taxable year, which shall be prescribed by the Secretary and which shall be in such form as he determines appropriate. In the table so prescribed, the amounts of the tax shall be computed on the basis of the rates prescribed by section 1.

(2) Ceiling amount defined

For purposes of paragraph (1), the term “ceiling amount” means, with respect to any taxpayer, the amount (not less than $20,000) determined by the Secretary for the tax rate category in which such taxpayer falls.

(3) Authority to prescribe tables for taxpayers who itemize deductions

The Secretary may provide that this section shall apply also for any taxable year to individuals who itemize their deductions. Any tables prescribed under the preceding sentence shall be on the basis of taxable income.

(b) Section inapplicable to certain individuals

This section shall not apply to-

(1) an individual making a return under section 443(a)(1) for a period of less than 12 months on account of a change in annual accounting period, and

(2) an estate or trust.

(c) Tax treated as imposed by section 1

For purposes of this title, the tax imposed by this section shall be treated as tax imposed by section 1.

(d) Taxable income

Whenever it is necessary to determine the taxable income of an individual to whom this section applies, the taxable income shall be determined under section 63.

(e) Cross reference

For computation of tax by Secretary, see section 6014.

(Aug. 16, 1954, ch. 736, 68A Stat. 8 ; Pub. L. 88–272, title III, §301(a), Feb. 26, 1964, 78 Stat. 129 ; Pub. L. 91–172, title VIII, §803(c), Dec. 30, 1969, 83 Stat. 684 ; Pub. L. 94–12, title II, §201(c), Mar. 29, 1975, 89 Stat. 29 ; Pub. L. 94–455, title V, §501(a), Oct. 4, 1976, 90 Stat. 1558 ; Pub. L. 95–30, title I, §101(b), May 23, 1977, 91 Stat. 131 ; Pub. L. 95–600, title IV, §401(b)(1), Nov. 6, 1978, 92 Stat. 2867 ; Pub. L. 95–600, title II, §202(g), as added Pub. L. 96–222, title I, §108(a)(1)(A), Apr. 1, 1980, 94 Stat. 223 ; Pub. L. 96–222, title I, §108(a)(1)(E), Apr. 1, 1980, 94 Stat. 225 ; Pub. L. 97–34, title I, §§101(b)(2)(B), (C), (c)(2)(A), 121(c)(3), Aug. 13, 1981, 95 Stat. 183 , 197; Pub. L. 99–514, title I, §§102(b), 141(b)(1), Oct. 22, 1986, 100 Stat. 2102 , 2117.)

AMENDMENTS

1986-Subsec. (a). Pub. L. 99–514, §102(b), substituted subsec. (a) for former subsec. (a) which read as follows:

“(1) In general.-In lieu of the tax imposed by section 1, there is hereby imposed for each taxable year on the tax table income of every individual whose tax table income for such year does not exceed the ceiling amount, a tax determined under tables, applicable to such taxable year, which shall be prescribed by the Secretary and which shall be in such form as he determines appropriate. In the tables so prescribed, the amounts of tax shall be computed on the basis of the rates prescribed by section 1.

“(2) Ceiling amount defined.-For purposes of paragraph (1), the term “ceiling amount” means, with respect to any taxpayer, the amount (not less than $20,000) determined by the Secretary for the tax rate category in which such taxpayer falls.

“(3) Certain taxpayers with large number of exemptions.-The Secretary may exclude from the application of this section taxpayers in any tax rate category having more than the number of exemptions for that category determined by the Secretary.

“(4) Tax table income defined.-For purposes of this section, the term ‘tax table income’ means adjusted gross income-

“(A) reduced by the sum of-

“(i) the excess itemized deductions, and

“(ii) the direct charitable deduction, and

“(B) increased (in the case of an individual to whom section 63(e) applies) by the unused zero bracket amount.

“(5) Section may be applied on the basis of taxable income.-The Secretary may provide that this section shall be applied for any taxable year on the basis of taxable income in lieu of tax table income.”

Subsec. (b). Pub. L. 99–514, §141(b)(1), struck out par. (1) which read: “an individual to whom section 1301 (relating to income averaging) applies for the taxable year,” and redesignated pars. (2) and (3) as (1) and (2), respectively.

1981-Subsec. (a)(1). Pub. L. 97–34, §101(b)(2)(B), inserted “and which shall be in such form as he determines appropriate” after “Secretary”.

Subsec. (a)(4)(A). Pub. L. 97–34, §121(c)(3), substituted “reduced by the sum of (i) the excess itemized deductions, and (ii) the direct charitable deduction” for “reduced by the excess itemized deductions”.

Subsec. (a)(5). Pub. L. 97–34, §101(b)(2)(C), added par. (5).

Subsec. (b)(1). Pub. L. 97–34, §101(c)(2)(A), substituted “an individual to whom section 1301 (relating to income averaging) applies for the taxable year” for “an individual to whom (A) section 1301 (relating to income averaging), or (B) section 1348 (relating to maximum rate on personal service income), applies for the taxable year”.

1980-Subsec. (b)(1). Pub. L. 96–222 redesignated subpars. (B) and (C) as (A) and (B), respectively, and struck out former subpar. (A) which made reference to section 911 (relating to earned income from sources without the United States).

1978-Subsec. (b)(1). Pub. L. 95–600 struck out subpar. (B) which related to the alternative capital gains tax under section 1201 of this title, and redesignated subpars. (C) and (D) as (B) and (C), respectively.

1977-Pub. L. 95–30 struck out “having taxable income of less than $20,000” after “individuals” in section catchline. Subsec. (a). Pub. L. 95–30 designated existing provisions as par. (1), substituted “tax table income” for “taxable income” and “does not exceed the ceiling amount” for “does not exceed $20,000”, and added pars. (2) to (4). Subsecs. (b) to (e). Pub. L. 95–30 added subsec. (b), redesignated former subsec. (b) as (c), and added subsecs. (d) and (e).

1976-Pub. L. 94–455 designated existing provisions as subsec. (a), substituted provision relating to taxable income for such year does not exceed $20,000 for provision relating to adjusted gross income for such year is less than $15,000 and who has elected for such year to pay the tax imposed by this section, struck out “or his delegate” after “Secretary”, “beginning after Dec. 31, 1969” after “each taxable year”, struck out provision requiring computation of taxable income by using standard deduction, and added subsec. (b).

1975-Pub. L. 94–12 substituted “$15,000” for “$10,000”.

1969-Pub. L. 91–172 raised the individual gross income limit of $5,000 to $10,000 for exercising the option and substituted provision that the tax has to be determined under tables to be prescribed by the Secretary or his delegate for tables of tax rates for single persons, heads of household, married persons filing joint returns, married persons filing separate returns with 10 per cent standard deduction and married persons filing separate returns with minimum standard deduction.

1964-Pub. L. 88–272 substituted optional tax tables covering five categories for taxable years beginning on or after Jan. 1, 1964, and before Jan. 1, 1965, and for years beginning after Dec. 31, 1964, for a single general table.

Effective Date of 1986 Amendment

Amendment by Pub. L. 99–514 applicable to taxable years beginning after Dec. 31, 1986, see section 151(a) of Pub. L. 99–514, set out as a note under section 1 of this title.

Effective Date of 1981 Amendment

Amendment by section 101(c)(2)(A) of Pub. L. 97–34 applicable to taxable years beginning after Dec. 31, 1981, see section 101(f)(1) of Pub. L. 97–34, set out as a note under section 1 of this title.

Amendment by section 121(c)(3) of Pub. L. 97–34 applicable to contributions made after Dec. 31, 1981, in taxable years beginning after such date, see section 121(d) of Pub. L. 97–34, set out as a note under section 170 of this title.

Effective Date of 1980 Amendment

Pub. L. 96–222, title I, §108(a)(2), Apr. 1, 1980, 94 Stat. 225 , provided that:

“(A) In general.-Except as provided in subparagraph (B), the amendments made by paragraph (1) [amending this section and sections 119, 911, and 913 of this title] shall take effect as if included in the Foreign Earned Income Act of 1978 [Pub. L. 95–615].

“(B) Paragraph (1)(E).-The amendment made by paragraph (1)(E) [amending this section] shall apply to taxable years beginning after December 31, 1978.”

Effective Date of 1978 Amendment

Amendment by section 401(b)(1) of Pub. L. 95–600 applicable to taxable years beginning after Dec. 31, 1978, see section 401(c) of Pub. L. 95–600, set out as a note under section 1201 of this title.

Effective Date of 1977 Amendment

Amendment by Pub. L. 95–30 applicable to taxable years beginning after Dec. 31, 1976, see section 106(a) of Pub. L. 95–30, set out as a note under section 1 of this title.

Effective Date of 1976 Amendment

Pub. L. 94–455, title V, §508, Oct. 4, 1976, 90 Stat. 1569 , provided that: “Except as otherwise provided, the amendments made by this title [enacting section 44A, amending this section and sections 36, 37, 41, 42, 46, 50A, 104, 144, 213, 217, 904, 1211, 1304, 3402, 6014, and 6096, enacting provisions set out as notes under sections 105, 8022, and repealing sections 4 and 214 of this title] shall apply to taxable years beginning after December 31, 1975.”

Effective and Termination Dates of 1975 Amendment

Pub. L. 94–12, title II, §209(a), Mar. 29, 1975, 89 Stat. 35 , as amended by Pub. L. 94–164, §2(e), Dec. 23, 1975, 89 Stat. 972 , provided that: “The amendments made by sections 201, 202(a), and 203 [enacting section 42 of this title and amending this section and sections 56, 141, 6012, and 6096 of this title] shall apply to taxable years ending after December 31, 1974. The amendments made by sections 201(a) and 202(a) [amending section 141 of this title] shall cease to apply to taxable years ending after December 31, 1975; those made by sections 201(b), 201(c), and 203 [enacting section 42 of this title and amending this section and sections 56, 6012, and 6096 of this title] shall cease to apply to taxable years ending after December 31, 1976.”

Effective Date of 1969 Amendment

Amendment by Pub. L. 91–172 applicable to taxable years beginning after Dec. 31, 1969, see section 803(f) of Pub. L. 91–172, set out as a note under section 1 of this title.

Effective Date of 1964 Amendment

Pub. L. 88–272, title III, §301(c), Feb. 26, 1964, 78 Stat. 140 , as amended by Pub. L. 99–514, §2, Oct. 22, 1986, 100 Stat. 2095 , provided that: “Except for purposes of section 21 of the Internal Revenue Code of 1986 [formerly I.R.C. 1954] (relating to effect of changes in rates during a taxable year), the amendments made by this section [amending this section and sections 4 and 6014 of this title] shall apply to taxable years beginning after December 31, 1963.”

https://uscode.house.gov/view.xhtml?req=(title:26 section:3 edition:prelim) OR (granuleid:USC-prelim-title26-section3)&f=treesort&edition=prelim&num=0&jumpTo=true

26 USC 6014: Income tax return-tax not computed by taxpayer

Text contains those laws in effect on May 4, 2016

Title 26-INTERNAL REVENUE CODE

Subtitle F-Procedure and Administration

CHAPTER 61- INFORMATION AND RETURNS

Subchapter A- Returns and Records

PART II- TAX RETURNS OR STATEMENTS

Subpart B- Income Tax Returns

- 6014. Income tax return-tax not computed by taxpayer

(a) Election by taxpayer

An individual who does not itemize his deductions and who is not described in section 6012(a)(1)(C)(i), whose gross income is less than $10,000 and includes no income other than remuneration for services performed by him as an employee, dividends or interest, and whose gross income other than wages, as defined in section 3401(a), does not exceed $100, shall at his election not be required to show on the return the tax imposed by section 1. Such election shall be made by using the form prescribed for purposes of this section. In such case the tax shall be computed by the Secretary who shall mail to the taxpayer a notice stating the amount determined as payable.

(b) Regulations

The Secretary shall prescribe regulations for carrying out this section, and such regulations may provide for the application of the rules of this section-

(1) to cases where the gross income includes items other than those enumerated by subsection (a),

(2) to cases where the gross income from sources other than wages on which the tax has been withheld at the source is more than $100,

(3) to cases where the gross income is $10,000 or more, or

(4) to cases where the taxpayer itemizes his deductions or where the taxpayer claims a reduced standard deduction by reason of section 63(c)(5).

Such regulations shall provide for the application of this section in the case of husband and wife, including provisions determining when a joint return under this section may be permitted or required, whether the liability shall be joint and several, and whether one spouse may make return under this section and the other without regard to this section.

(Aug. 16, 1954, ch. 736, 68A Stat. 736 ; Pub. L. 88–272, title II, §201(d)(14), title III, §301(b)(2), Feb. 26, 1964, 78 Stat. 32 , 140; Pub. L. 91–172, title VIII, §803(d)(1), title IX, §942(a), Dec. 30, 1969, 83 Stat. 684 , 726; Pub. L. 94–455, title V, §§501(b)(8), (9), 503(b)(2), (3), title XIX, §1906(b)(13)(A), Oct. 4, 1976, 90 Stat. 1559 , 1562, 1834; Pub. L. 95–30, title I, §101(d)(13), (14), May 23, 1977, 91 Stat. 134 ; Pub. L. 99–514, title I, §104(b)(16), Oct. 22, 1986, 100 Stat. 2106 .)

AMENDMENTS

1986-Subsec. (a). Pub. L. 99–514, §104(b)(16)(A), substituted “who is not described in section 6012(a)(1)(C)(i)” for “who does not have an unused zero bracket amount (determined under section 63(e))”.

Subsec. (b)(4). Pub. L. 99–514, §104(b)(16)(B), amended par. (4) generally, substituting “where the taxpayer claims a reduced standard deduction by reason of section 63(c)(5)” for “has an unused zero bracket amount”.

1977-Subsec. (a). Pub. L. 95–30, §101(d)(13), substituted “An individual who does not itemize his deductions and who does not have an unused zero bracket amount (determined under section 63(e)), whose gross income” for “An individual entitled to take the standard deduction provided by section 141 (other than an individual described in section 141(e)) whose gross income” and struck out “and shall constitute an election to take the standard deduction” after “Such election shall be made by using the form prescribed for purposes of this section”.

Subsec. (b)(4). Pub. L. 95–30, §101(d)(14), substituted “itemizes his deductions or has an unused zero bracket amount” for “does not elect the standard deduction or where the taxpayer elects the standard deduction but is subject to the provision of section 141(e) (relating to limitations in case of certain dependent taxpayers)”.

1976-Subsec. (a). Pub. L. 94–455, §§501(b)(8), 503(b)(2), 1906(b)(13(A), substituted “entitled to take the standard deduction provided by section 141 (other than an individual described in section 141(e))” for “entitled to elect to pay the tax imposed by section 3” and “take the standard deduction” for “pay the tax imposed by section 3” and struck out provision relating to disallowance of section 37 credit in determination of tax imposed by section 3 of this title, and struck out “or his delegate” after “Secretary”.

Subsec. (b). Pub. L. 94–455, §§501(b)(9), 503(b)(3), 1906(b)(13)(A), struck out an introductory provision, “or his delegate” after “Secretary”, redesignated former par. (5) as (4), and as so redesignated, inserted reference to where the taxpayer elects the standard deduction but is subject to the provisions of section 141(e) (relating to limitations in case of certain dependent taxpayers). Former par. (4), which related to cases where the taxpayer is entitled to credit provided by section 37 of this title, was struck out.

1969-Subsec. (a). Pub. L. 91–172, §803(d)(1), raised the individual gross income limit of $5,000 to $10,000 for exercising the option to pay the tax under section 3 of this title, and struck out provisions relating to heads of household, surviving spouses and married individuals filing separate returns.

Subsec. (b). Pub. L. 91–172, §942(a), substituted provisions authorizing the Secretary to promulgate regulations to compute the tax in cases where the gross income is $10,000 or more, where the gross income from sources other than wages on which the tax has been withheld at the source is more than $100, where the taxpayer is entitled to a credit under section 37 of this title, or where the taxpayer does not elect the standard deduction, for provisions authorizing the computation of the tax in cases where the gross income is $5,000 but not more than $5,200, or where the gross income from sources other than wages on which the tax has been withheld at the source is more than $100, but not more than $200.

1964-Subsec. (a). Pub. L. 88–272 struck out “34 or” before “37 shall not be allowed”, and inserted provision that in case of a married individual filing a separate return and electing benefits of this subsection, neither Table V in section 3(a) nor Table V in section 3(b) shall apply.

Effective Date of 1986 Amendment

Amendment by Pub. L. 99–514 applicable to taxable years beginning after Dec. 31, 1986, see section 151(a) of Pub. L. 99–514, set out as a note under section 1 of this title.

Effective Date of 1977 Amendment

Amendment by Pub. L. 95–30 applicable to taxable years beginning after Dec. 31, 1976, see section 106(a) of Pub. L. 95–30, set out as a note under section 1 of this title.

Effective Date of 1969 Amendment

Amendment by section 803(d)(1) of Pub. L. 91–172 applicable to taxable years beginning after Dec. 31, 1969, see section 803(f) of Pub. L. 91–172, set out as a note under section 1 of this title.

Pub. L. 91–172, title IX, §942(b), Dec. 30, 1969, 83 Stat. 727 , provided that: “The amendment made by subsection (a) [amending this section] shall apply to taxable years beginning after December 31, 1969.”

Effective Date of 1964 Amendment

Amendment by section 201(d)(14) of Pub. L. 88–272 applicable with respect to dividends received after Dec. 31, 1964, in taxable years ending after such date, see section 201(e) of Pub. L. 88–272, set out as a note under section 22 of this title.

Amendment by section 301(b)(2) of Pub. L. 88–272 applicable to taxable years beginning after Dec. 31, 1963, except for purpose of section 21, see section 301(c) of Pub. L. 88–272, set out as a note under section 3 of this title.

https://uscode.house.gov/view.xhtml?req=(title:26 section:6014 edition:prelim) OR (granuleid:USC-prelim-title26-section6014)&f=treesort&edition=prelim&num=0&jumpTo=true

- §5. Cross references relating to tax on individuals

- §12. Cross references relating to tax on corporations

- §140. Cross references to other Acts

- §153. Cross references

- §224. Cross reference

- §885. Cross references

- §1023. Cross references

- §1061. Cross references

- §1505. Cross references

- §4084. Cross references

- §4227. Cross reference

- §4405. Cross references

- §4414. Cross references

- §4484. Cross references

- §5003. Cross references to exemptions, etc.

- §5045. Cross references

- §5067. Cross references

- §5182. Cross references

- §5244. Cross references

- §5403. Cross references

- §5663. Cross reference

- §6040. Cross references

- §6117. Cross references

- §6207. Cross references see chapter 66

- §6216. Cross references

- §6216. Cross references

- §6327. Cross references

- §6344. Cross references

- §6344. Cross references

- §6422. Cross references

- §6504. Cross references

- §6515. Cross references

- §6533. Cross references

- §6612. Cross references

- §7012. Cross references

- §7103. Cross references– Others provisions for bonds

- §7124. Cross references

- §7328. Cross references

- §7410. Cross references

- §7437. Cross references

- §7487. Cross references

- §7613. Cross references

- §7655. Cross references